Startup Jedi

We talk to startups and investors, you get the value.

In our previous article, we talked in detail about the convertible note but there are many other popular ways of raising investments — SAFE and KISS.

SAFE and KISS are derivatives of convertible note for simplifying the investment process. In this article, I will try to completely disclose the SAFE functional.

Startup Jedi

We talk to startups and investors, you get the value.

SAFE is a another way of raising investments at the early stages. It’s quite similar to a convertible note, but with one exception — SAFE isn’t a loan, it is a equity investing, so there is no Interest rate, Maturity Date and Maturity Cap. It is more simple and it has an impact on the number of spelt conditions and the investor’s curtailed rights.

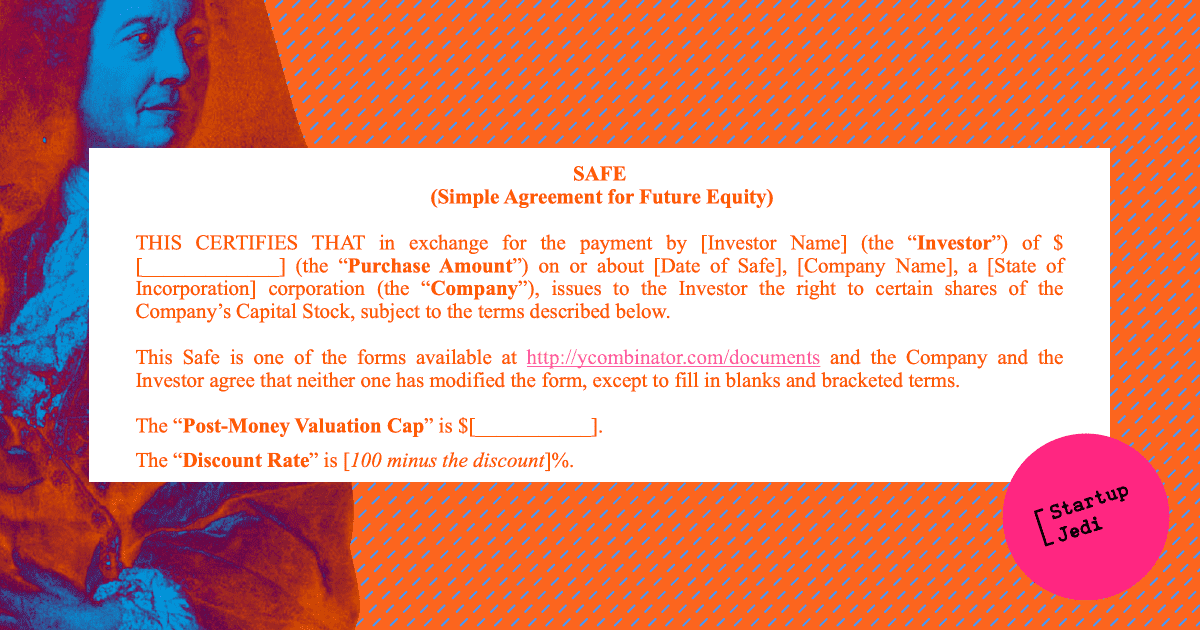

It is believed, that SAFE shouldn’t be changed, and even in a document from Y Combinator there is a point that states “This Safe is one of the forms available at http://ycombinator.com/documents and the Company and the Investor agree that neither one has modified the form, except to fill in blanks and bracketed terms.”

A bit of history:

Back in 2013, Y Combinator announced the first version of SAFE — Pre-money SAFE, as an easy and quick way of getting small investments before the Equity round (usually, before Round A). And then up to 2018, rounds have become bigger so it was hard for investors to count what % of the company they have, and startups stopped understanding the dilution of shares, and that’s why a new updated version of SAFE 2.0 came off — Post-money SAFE. The additional feature of the new updated version was in fact that the investor’s share in SAFE wasn’t diluting by other SAFE’s until the Equity round.

...

YC offers to stop inventing the wheel and start using 4 trustworthy variants (you can find them on the YC website by following the link https://www.ycombinator.com/documents):

Safe: Valuation Cap, no Discount

Safe: Discount, no Valuation Cap

Safe: Valuation Cap and Discount

Safe: MFN (most favoured nation), no Valuation Cap, no Discount

and an optional condition — Pro-Rata Side Letter.

The main and only conditions are spelt here and depend on the SAFE type.

Valuation Cap — the limit of the company’s valuation in the Equity round, so that there is not too much dilution of the investor’s share. It is a standard practice in the US to set Cap at $5M, but in the CIS region's reality Cap is $1M-2M.

Discount Rate — a discount for buying shares when converting investments into company shares. It is counted as 100% minus the discount percentage. For example, a 30% discount should be recorded as a Discount Rate of 70%, usually, a discount is in the range of 10–30%.

On the Equity round, when shares are distributed among investors, the price per share is calculated according to the Valuation Cap and Discount Rate, and, obviously, the lower one is the chosen one.

SAFE MFN (most-favoured-nation) type means that we write down only the investments sum. If a startup raises more investments with SAFE in which Valuation Cap and/ or Discount Rate are already prescribed, then an investor with SAFE MFN can join under the same conditions. Truth be told, this is a one-time thing, it will not be possible to choose the conditions more than once, and if suddenly the startup no longer raises investments with SAFE, then investments will have to be converted into shares according to the conditions of the Equity round, and it’s clearly not great.

Pro-rata Side Letter is an additional document the sign of which allows the investor to invest up to the per cent he had before the dilution. Now in plain English: if the investor before the Equity round, i.e. before the dilution of the shares, “acquired” 10% of the company, and after the Equity round he had 8% left, then he has the right to invest additional investmnets so to have 10% of the company in the Equity round.

...

The document itself contains 5 pages and 5 chapters:

1. Events

Equity Financing. On the Equity round, the investment is automatically converted into a share using Preferred Stocks, taking into account the conditions specified in the SAFE for the Valuation Cap and/ or Discount (depending on which condition the price per share is lower) or MFN.

Liquidity Event — for M&A, IPO, Direct listing before Equity round. Here the investor either returns the investment or converts it into shares at the Valuation Cap and then sells.

Dissolution Event. When a company is closed, the investment must be returned. But, as a rule, if a startup closes, it has no money to return.

Liquidation Priority (Priority of payments for Liquidity Event and Dissolution Event). When a company is sold or closed, the SAFE investor gets the investment back after other lenders and convertible loans, but before the founders and employees.

Termination. In theory, SAFE can run indefinitely until the company raises an Equity round.

2. Definitions. The glossary.

3. Company Representations. In this chapter, the startup proves that:

The company is registered as a legal entity (most often the state of Delaware is of interest (Stripe Atlas for help),

The company’s board of directors approved SAFE,

The signed SAFE does not contradict any agreements signed in the past,

No additional permission is required from anyone to sign SAFE,

Intellectual property has not been stolen.

4. Investor Representations. In this chapter, the investor proves, that:

If he represents a fund or trust, he has the authority to sign SAFE,

The investor is accredited (in the United States, an accredited investor is the one having assets for at least $1 million (not including the cost of the main residence), the annual income of more than $200K for the last 2 years or annual income with a spouse of more than $300K for the last 2 years).

5. Miscellaneous. Hereby it is stated that:

SAFE can only be changed in written form with signatures of directors and the majority of the investors — holders of SAFEs with the same Valuation Cap or Discount Rate,

Important notes can be sent by email,

Until the conversion of SAFE in the Equity round takes place, the investor does not have the right of shareholders under the Shareholders agreement,

An investor can't resell SAFE to someone, just as a startup can't transfer SAFE to another startup,

If any SAFE position is invalidated by a judge, it will not 'kill' the entire SAFE, but only that one position,

The state is specified, according to the laws of which the court will be conducted, even if the court is in another state, it will be obliged to consider the case according to the laws of the state specified in the SAFE,

And for taxes — SAFE is not a debt, it is an equity investment tool.

Always track the Cap table and don’t forget to include SAFE and other investment tools.

For calculations and tracking the Cap table, you can old-fashionably use Excel (thank God, we have tons of templates on the Internet), but it is better to use Carta service (but this point works only if you are an American company) or an analogue.

All calculations are stated in detail on Y Combinator’s website as well as all SAFE templates.

Minuses:

The only way to make money is to pray that the startup will survive, close the Equity round and give a share. Otherwise, if the startup dies before the Equity round, the investor gets nothing (which is not so unexpected for the venture market);

There is a very small likelihood that the startup raises investments with SAFE and everything flows so well for it that it doesn't raise the Equity round or sells the company. Accordingly, you will not receive a share.

Venture in da house!

Facebook: facebook.com/StartupJedi/

Telegram: t.me/Startup_Jedi

Twitter: twitter.com/startup_jedi

Comments